%201.svg "cancel (1) 1")

In February, Federal Treasurer Jim Chalmers made the call to back the Foreign Investment Review Board (FIRB) recommendation to reject a Chinese-linked fund’s increased equity stake in an emerging Australian critical minerals developer, ASX-listed Northern Minerals. Northern Minerals is set to mine the rare earth dysprosium, used as an additive in neodymium magnets for electric vehicle motors.

Not an easy call when it involves rejecting an investment by Australia’s largest trade partner, even as Senator Penny Wong is making headway in the Albanese government’s efforts to improve our relationship with China after a dramatic deterioration over recent years. But strategically, the decision is a sensible call. The context is Chalmers’ approval in the same month of another Chinese firm taking a much larger strategic stake in a new $2bn iron ore mine in partnership with Rio Tinto.

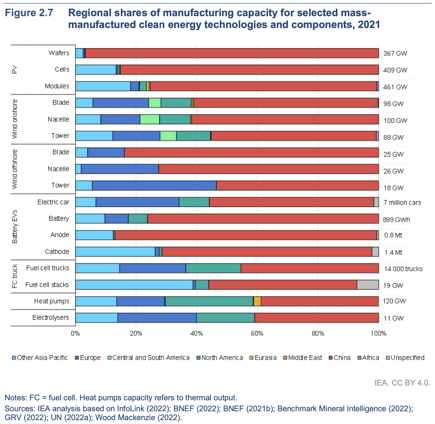

The global context is also important. China absolutely dominates almost all energy transition sectors, be that solar and wind installations, solar and wind supply chain manufacturing, batteries, electric vehicles (EV), green hydrogen and refining of critical minerals and metals. The IEA estimates China’s global market share in 2021 in refining lithium is 60%, nickel is 40%, cobalt 60%, batteries 75%, and anodes for batteries 85%, while EV manufacturing is 55%. China also deployed US$546bn in energy transition investments in 2022, four times that of the US, according to BloombergNEF (BNEF).

Figure: Regional Share of Manufacturing Capacity for Clean Energy Technologies and Components 2021:

Source: IEA Clean Energy Technologies Report 2023

Putin’s invasion of Ukraine and the resulting trade sanctions against Russia gave the world a stark reminder of the critical importance of energy security, and global supply chain security. The IEA reports Russia in 2020 was the world’s #3 nickel, #2 cobalt, #4 graphite and #1 palladium supplier.

Rising trade and geopolitical tensions between North America and China have seen growing trade barriers and tariffs, culminating in the massive US Inflation Reduction Act (IRA) subsidy program overtly preferencing US onshore manufacturing, and overtly supporting allies with which the US has established free trade agreements (like Australia).

After the Treasurer accepted FIRB’s recommendation to approve China Baowu Steel Group’s involvement in the $2bn Western Range iron ore project in Western Australia (WA) in partnership with Rio Tinto, he rejected Chinese-linked investment fund Yuxiao Fund’s request to increase its stake in Northern Minerals Limited from just under 10% to 19.9%.

Northern Minerals operates the Browns Range pilot mine in WA's northern Tanami region, aiming to become the first substantial producer of dysprosium outside China. Northern Minerals has been pushing to develop a commercial-scale beneficiation plant that would provide a reliable alternative source of both dysprosium and another critical mineral – terbium – with a feasibility study due 3QCY2023 regarding a processing plant reported to cost up to $300m.

While Northern Minerals has a strategic partnership with ASX-listed Iluka Resources, the rejection of Yuxiao’s bid highlights the Climate Capital Forum’s key recommendation that patient public equity capital from the Future Fund be invested to support critical minerals projects as a strategic national priority.

China already dominates the world’s processing of rare earths, and controls a large part of the mining of rare earths globally. Australia is really well positioned to provide a strategic alternative at scale to China in rare earth mining, and potentially in refining onshore.

For example, the Future Fund could help ensure this business remains majority Australian owned, and hence pays Australian corporate tax once operational. It could ensure best ESG practices, and “crowd-in” CEFC/ARENA funding for a hybrid renewable energy-powered microgrid. This would incorporate embodied decarbonisation into our refined critical mineral exports by leveraging our world-leading low cost zero emissions renewables to power processing onshore.

Australia’s global role is set to expand significantly with the federal government’s Export Finance Australia committing to a $1.2bn of non-recourse, long dated loan to Iluka Resources to develop a rare earth oxide refinery at Eneabba, WA to produce 4ktpa of NdPr (neodymium and praseodymium) products. The government has also encouraged Lynas Rare Earths to invest $500m to expand its Mt Weld rare earth mine and concentrate facility in Kalgoorlie, WA.

Climate Energy Finance advocates a continued pragmatic approach to rebuilding our relationship with our foremost trade partner.

In contrast, the events last month in the US highlight the growing geopolitical risk for firms in strategically important industries.

Microvast Holdings Inc. saw their shares plunge 33% year-to-date 2023 as a direct result of the US Department’s Office of Intelligence and Counterintelligence questioning their extensive China operations and links to the Chinese government, putting at risk their access to a US$200m DoE loan grant for proposed US lithium battery manufacturing investments, even as the company emphasised it is a publicly traded American firm with no Chinese government ownership.

October 2022 saw the Canadian government force Chinese investors to divest from certain Canadian critical mineral companies. Canada’s new policy limits transactions between domestic critical mineral projects and foreign state-owned enterprises while incentivizing investments from "partners that share our interests and values." Canada ordered three Chinese companies to divest minority stakes in three lithium developers. Under the order, Sinomine Resource Group Co. Ltd., Chengxin Lithium Group Co. Ltd. and Zangge Mining Company Ltd. were required to divest their respective interests in Power Metals Corp., Lithium Chile Inc. and Ultra Lithium Inc.

There is a clear and pressing need for a well thought through strategic Australian response to the US IRA. China has been moving strategically for several decades, and even in the last two months has lined up a reported US$132bn in strategic moves to align with critical minerals and metals developments in Indonesia. A US$1bn strategic alignment with Bolivia in lithium was announced in February 2023. Both are direct new world scale competitors to Australia in this global technology and investment race.

In March, Climate Energy Finance launched a new report “A Critical Minerals Value-Adding Superpower: Mapping Australia’s ‘once in a century’ opportunity to lead the world in new economy minerals mining and renewables-powered onshore refining and manufacturing pre-export”. The investment, employment and export opportunities are huge. The opportunities for Australia to export embodied decarbonisation by value-adding our critical minerals and metals pre-export powered using our renewables are enormous.

A global investment race is already well underway. A strategic national agenda is clearly needed for Australia to maximise our opportunities.

We recommend patient public debt, equity, infrastructure, grant, export credit and VC funding be accelerated to deliver on this national objective, crowding in our brilliant competitive advantage of a $3.3 trillion pool in superannuation increasingly looking to play a constructive role as well.

Australia should continue to welcome global capital partnerships, but majority Australian ownership has very positive strategic benefits for us, particularly in light of multinationals like Chevron and BP failing to pay any material corporate tax here. We need to share the burden of funding, and then repaying some of the previous government’s $1 trillion federal debt burden that we now collectively carry.

.png)

Creating clarity during the energy transition.

Get a different perspective on energy with our monthly newsletter.