%201.svg "cancel (1) 1")

If I had a dollar for every time someone asked me where FCAS prices were headed… I’d probably have enough to purchase a regular-sized latte in a capital city. So in the interests of keeping my caffeine consumption down, let’s talk FCAS.

The Markets

The Frequency Control Ancillary Services (FCAS) markets are a series of ten markets used to manage the frequency of the NEM.

There are eight Contingency FCAS markets, whose purpose is to arrest, halt and restore the system frequency to 50 Hz in the event of a contingency event. A contingency event is typically the sudden trip of a large thermal generator or loss of a transmission line which causes the frequency to deviate outside of the normal operating range (49.85 - 50.15 Hz).

FCAS Raise markets manage reductions in frequency, and the Lower services manage increases.

There are four markets each for Contingency Raise and Lower based on the speed of response required – Very Fast (1 second response), Fast (6 second), Slow (60 second) and Delayed (5 minute). Eligible assets can simultaneously participate in all or some of these markets.

Batteries – including those in virtual power plants – and interruptible loads (demand response) are currently the only assets registered to participate in all four markets; traditional thermal and hydroelectric generators participate in the remaining markets, depending on their control systems and speed of response.

The Regulation markets on the other hand consist of a single Raise and Lower service each, used to maintain the frequency within the normal operating range on an ongoing basis. If the contingency markets are a handbrake to arrest sudden large deviations in the system frequency, the Regulation markets are a steady hand constantly nudging the system frequency back towards 50 Hz.

This difference is important – the Contingency services can be provided by a wide range of assets, whereas Regulation FCAS require control systems capable of sending and receiving signals from AEMO via SCADA every 4 seconds, effectively limiting participation to large utility-scale generation.

The FCAS markets have been a part of the NEM since inception, although the Very Fast 1 second markets were only introduced in October 2023.

Payments and Pricing

Like energy, each FCAS service is its own market, with a wholesale price varying every 5 minutes. Bidding is via 10 tranches with a floor of $0/MW/hr and a cap of $16,600/MW/hr, (higher if you’re reading this article after 1 July).

There is a unique regional price for each service, but in practice, the price is the same across all regions 90% of the time. However, when there is physical separation (or the risk of separation) between regions, very large price spikes can occur; this is mostly experienced in Tasmania, South Australia and Queensland.

Importantly, FCAS markets are capacity markets – payments are made on the basis of capacity made available, not the actual responses. In fact, actual responses play no role in setting prices.

One truism of FCAS prices is that the more difficult the service is to provide, the more valuable it is. This doesn’t hold true every hour of the day, but Regulation services are on average much more valuable than Fast services, which are more valuable than Slow services…

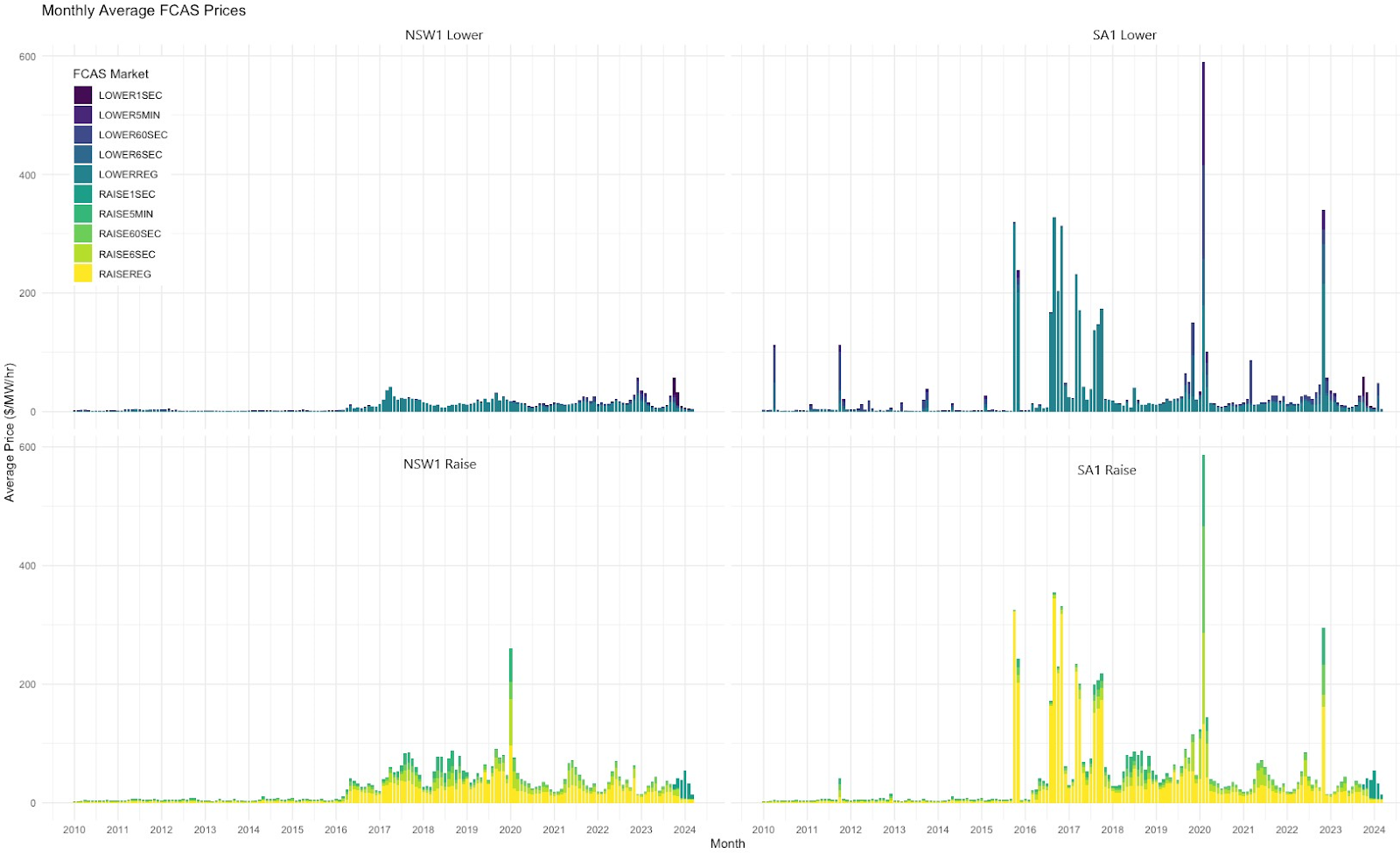

What have prices been doing?

If you had never heard of FCAS until recently, there’s good reason – although essential to keeping the grid running, the prices were very low. And the era of the big battery didn’t arrive until late 2017, when Neoen’s Hornsdale battery began operating, demonstrating the value that FCAS revenues could provide to energy-constrained resources.

The chart below shows two clear trends:

-

A significant uptick in early 2016 where prices increased on average by between 200-1,000% across the markets.

-

The significance of the price separation between a ‘stable’ region like NSW and a region which experiences physical separation across the Heywood interconnector into SA.

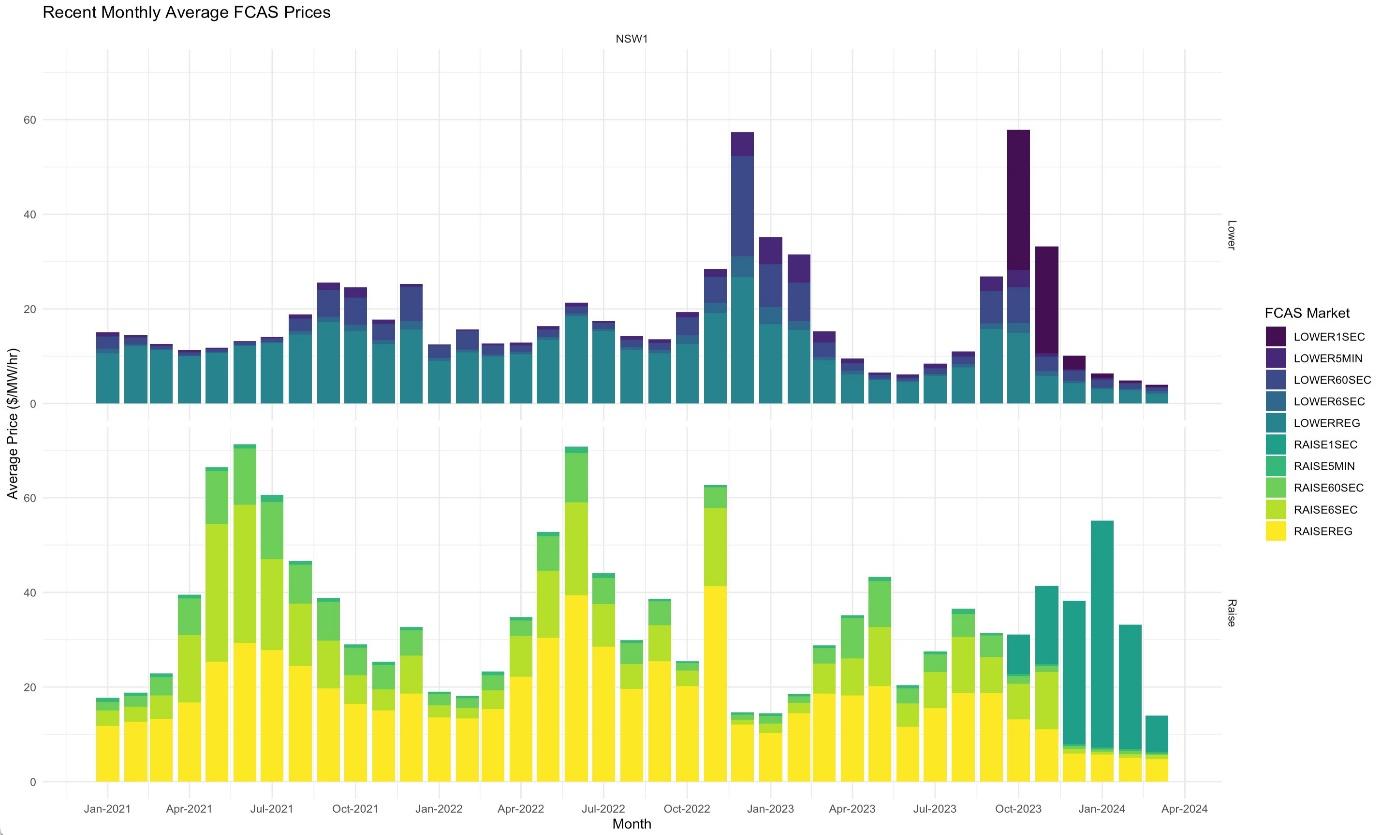

Let’s zoom in a little and look at more recent prices in the NSW region:

- We can see the explosive start of the Very Fast markets in October 2023, where Very Fast Contingency Lower was honestly ridiculous. Competition has inevitably collapsed the price in that market back to more sane levels.

- Fast Contingency Raise (6 second), the dominant revenue source for contingency-only players looks to have collapsed, although how related this is to the Very Fast Raise market will need more data to determine.

How about that coffee?

Let’s consider what the future of the NEM holds.

Headwinds

- Saturation of the contingency markets, as utility-scale batteries, small-scale batteries in VPPs and potentially even vehicle-to-grid collapse the prices

- Further potential saturation from wind and solar farms providing FCAS (they can do it!)

- The retirement of large thermal generators (primarily coal-fired) in coming years reduces the contingency size, which is directly correlated with contingency FCAS prices.

Tailwinds

- The retirement of large thermal generation however is also an opportunity – these plants have historically been the primary providers of FCAS.

- Retirement of large thermal generation will also yield less plants able to provide the specialised Regulation FCAS.

- Further reductions in ‘Load Relief’ (demand side inertia) increasing the volumes of FCAS procured, driving the price up.

- The rise of rooftop solar has created a new type of contingency on the grid, based around ramping speed; this will continue to grow in size.

- The introduction of the Very Fast markets was partly in response to this, and other new types of FCAS markets have been proposed previously. It wouldn’t be out of the question to see new ancillary services markets introduced in the future, which would likely buffer the value stack for assets like batteries.

Crosswinds?

- Historically Lower services have been easy to provide (a spinning turbine simply needs to spin a little slower), which yields a lower price. Batteries and interruptible loads have the oppositedynamics – batteries sit idle for significant periods of the day. Could this yield a flip in pricing?

Overall, if you had to ask me to earn my coffee, the sensible prediction is that FCAS prices must go down – there are too many participants able to readily provide the services. It would certainly be naïve to be modelling a long-term stream of revenue at today’s values.

However, the rate at which they fall and how low they go is a big unknown. FCAS prices have done a remarkable job of remaining fairly steady even as utility-scale batteries, VPPs and demand response have flooded into the market since 2017, so don’t predict that cliff just yet…

.png)

Creating clarity during the energy transition.

Get a different perspective on energy with our monthly newsletter.