%201.svg "cancel (1) 1")

By Tahlia Nolan, Joel Gilmore, and Jack Munro

Over the past 11 years, there has been a near-perfect correlation between natural gas prices and electricity prices in Australia’s National Electricity Market (NEM), regardless of the underlying supply-demand balance and despite gas plants only operating for a small percentage of the year.

A key question is whether this trend will continue into the future under conditions of extreme commodity prices and the transition to a net-zero emissions grid. We examine the underlying drivers of this correlation through analysis of the marginal price setter in the NEM’s dispatch engine, and develop a minimal model of the NEM with a “grid heat rate” concept that accurately captures historical price dynamics. We find the NEM’s energy-only market creates incentives for all participants to shadow price the marginal unit where possible, to maximise short-run revenues. Gas pricing therefore affects the bids of all units, and will continue to play a key role for as long as gas generators remain as peaking generation. Extrapolating forward, it is possible that grid heat rates, and hence the role of gas in pricing, will decline but will not disappear. Finally, we test this model against the extreme fuel and electricity prices observed in 2022 and consider the role of coal outages in driving extreme prices.

Domestic gas market fluctuations

Furthermore, in 2015 Australia established an east coast Liquified Natural Gas (LNG) export market for the first time, tripling aggregate demand for domestic gas (and dwarfing consumption by gas-powered generation). Initially, gas prices fell due to an excess of gas available from new fields developed ahead of the export market. Exporting then linked domestic and international gas markets, and coincided with limited domestic gas supply and an increase in the production cost of domestic gas (Atholia & Walker, 2021).

Subsequently, domestic gas prices fluctuated between $3/GJ and $10/GJ (and at times trading at over $50/GJ) over the cycle. Inevitably, higher fuel costs flowed through to the marginal running cost of domestic gas power generation (GPG) as existing gas contracts expired, new contracts were struck at materially higher prices (and some generators opted to take spot exposure). However, even contracted generators were known to sell gas back to the grid at spot prices rather than increasing electricity generation; effectively linking marginal running costs to the elevated spot gas prices.

The linking of Australia’s domestic gas market with international gas markets meant that surging fossil fuel prices in 2022 following the Russian invasion of Ukraine flowed through to the domestic commodity prices. The electricity spot and forward prices rose to record levels following the existing strong relationship between gas price and electricity prices.

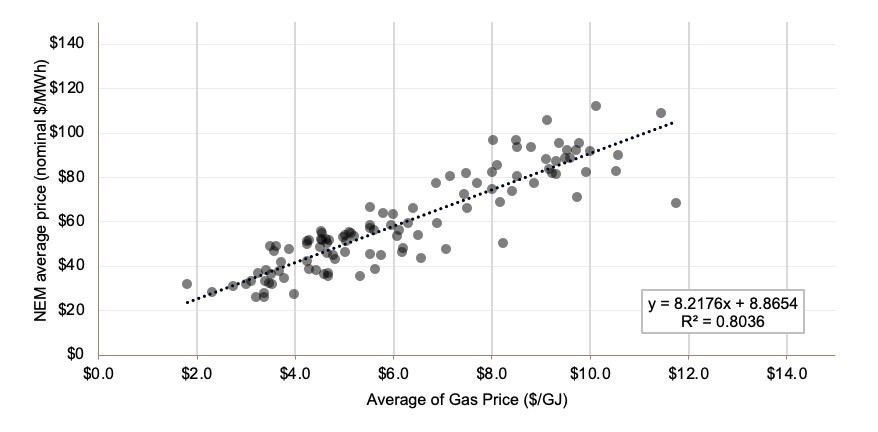

Figure 3 Monthly averaged NEM-wide volume weighted under-cap electricity prices vs average daily gas price STTM ex-ante 2012-2020

Figure 3 Monthly averaged NEM-wide volume weighted under-cap electricity prices vs average daily gas price STTM ex-ante 2012-2020

A framework for how gas prices will continue to drive wholesale spot prices in future

We developed a model to explain current and future trends for the role of gas in electricity pricing. Despite a declining role for gas peaking generation, they project gas prices will continue to drive wholesale spot prices by providing a benchmark price. This is important for storage technologies that do not have an easily definable marginal running cost, but also coal generators that regularly offer their capacity at prices above their marginal running costs. This means that even though gas contributes only 7-12% of Australia’s electricity, the gas price will therefore continue to impact both consumer and producer surpluses – leaving consumers exposed to sudden increases in gas price as has been seen in the UK and for short periods in the NEM market. We find gas prices have typically driven (directly or indirectly) 50-90% of pricing periods in the NEM.

This model quantifies the sensitivity of near-term electricity prices to gas prices, even as thermal coal and gas plant exit and new renewable and storage capacity enters. This approach can be used to calibrate more sophisticated strategic bidding or game theoretical pricing models and will help utilities and governments better quantify fuel price risks to consumers.

Advantages of a minimal model and why the Grid Heat Rate (GHR) is crucial

From 2012 to 2020, wholesale prices were tightly linked to energy prices, with a GHR (slope) of 8.2 GJ/MWh. That is, on average, for every $1/GJ increase in gas prices, electricity prices increased by $8.20/MWh. A minimal model of price setting behaviour confirms and explains this link in the NEM, but also highlights that there is variability year to year depending on projections, with annual Grid Heat Rates ranging from 5.5 to 9.8 GJ/MWh. This minimal model is effective at explaining the key drivers of this relationship, namely the opportunities for black coal units to set price and exercise transient market power. Over 2022, with the record levels of gas prices, coal prices and electricity prices, the predicted relationship by our minimal model was maintained. Again, this suggests our approach is robust across a broad range of market conditions.

A minimal model also allows insights that “black box” models struggle with, and can be used to inform more sophisticated models, including market simulation bidding behaviours. Although low wholesale prices in 2021 were initially regarded by some as evidence for a break in the relationship, the 2021 GHR (5.47 GJ/MWh) was not unusual in the history of the NEM. The lower GHR appears to have been driven by higher output from renewable and coal generation leading to greater competition amongst coal generators, and less opportunity for participants to exercise transient market power.

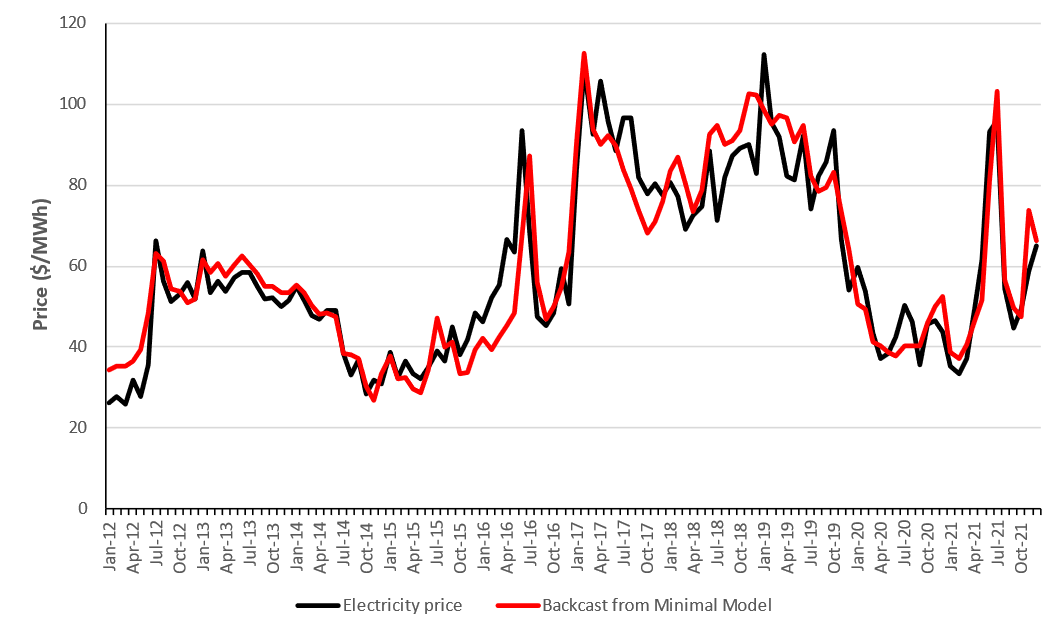

Figure 17 Backcast of monthly electricity prices using Backcast from Minimal Model against actual monthly weighted average electricity price in the NEM ($/MWh)

How GHR will evolve over time

The supply demand balance will undergo some significant changes over the coming decade. Coal generators will begin to retire in succession and new, never before seen loads will start to grow, such as electric mobility, electrification of heating, and electrolysers for green hydrogen production. Coal retirements will, at first, reduce the amount of time coal generators can set price, but could shift the strategic bidding opportunity for the remaining coal units as they become pivotal in meeting demand. However, the impact on consumers will depend on which type of generators take out the major price setting role and how responsive our new loads are.

If it is renewables and energy storage, as recent trends suggest, it is credible that those portfolios will grow to be able to shadow price the marginal price setting technology, e.g., gas. This is not necessarily a result of market power – for energy limited technologies, a shadow price for energy will necessarily be factored into bid decisions. (In particular, this is explicit in fully automated battery bidding programs, that co-optimise output across multiple timescales).

In a similar vein, emissions constraints may hasten the decline of coal, but may also increase opportunities for strategic bidding behaviours by units knowing that natural gas units have limited run hours. More detailed market models may benefit from benchmarking against the minimal model presented here. In the longer-term, reducing the impact on consumers of high gas prices relies on ensuring that competition remains at efficient levels.

This requires better coordination of coal outages, rapid uptake of renewable generation, and a sharp focus on the level of horizontal integration of market participants. This model suggests that if these issues had been addressed before the Russian invasion of Ukraine led to extreme gas prices, wholesale prices could have been up to 28% ($75/MWh) lower.

In the near-term, however, a GHR of 5-10 GJ/MWh is likely, and electricity consumers will remain exposed to swings in underlying commodity prices.

This is an extract from a more detailed paper. To read the full text, please click here.

.png)

Creating clarity during the energy transition.

Get a different perspective on energy with our monthly newsletter.